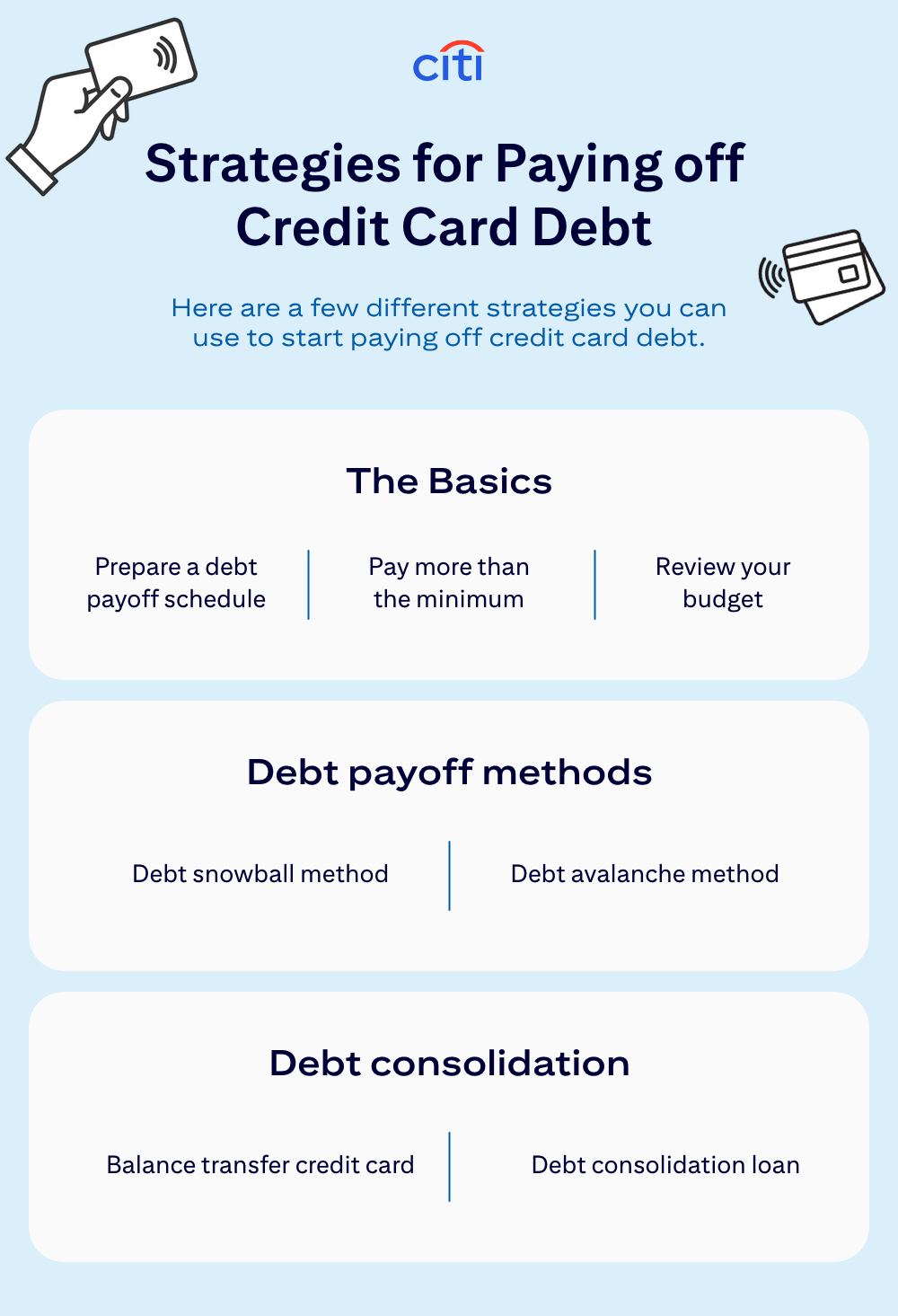

5. Credit card consolidation loan

If you have multiple credit card balances that are hard to manage, consider using a credit card consolidation loan.

This allows you to combine your existing credit card debts into a single loan, ideally with a lower interest rate than any of the interest rates applied to those existing debts. By consolidating, you simplify your debt repayment by focusing on one loan instead of juggling several credit card balances.

6. Pay more than the minimum

Another simple solution to handling credit card debt is to pay higher than your minimum monthly payment on your credit card balances. One strategy is to steadily increase the amount you pay on your balances each month to try to reduce your debt at a faster rate.

This strategy is ideal if you have fewer credit cards but higher balances. While you'll still need to make your minimum payments, paying more than the minimum can help lower your debt faster and reduce the risk of it becoming unmanageable. Keep in mind that interest will continue to grow over time, so the sooner you pay down your debt, the better.

7. Review your spending

If you're focused on paying off credit card debt, don't overlook the importance of tightening your budget for added financial flexibility. By reviewing your daily and monthly spending, you can identify areas to cut back, freeing up extra money to pay down your credit card balances faster.

How to avoid future credit card debt

Once you’ve paid off your credit card debt, come up with a plan to keep your finances manageable in the future. Whether that means more restrictive budgeting or paying off your balances faster, you’ll need to devise a plan going forward so that you can manage your debt properly.

If you continue to use credit cards, make sure to understand the terms. That way, you know when your minimum payments are due each month and the interest charges that can apply to transactions made with the cards.

Disclosure: This article is for educational purposes. It is not intended to provide legal, investment, or financial advice and is not a substitute for professional advice. It does not indicate the availability of any Citi product or service. For advice about your specific circumstances, you should consult a qualified professional.