With a Roth individual retirement account (IRA), you make post-tax contributions. That money can grow and be withdrawn tax-free if you meet certain requirements.

Roth IRAs can help you save for retirement and reach your financial goals. Here are 10 reasons to consider one.

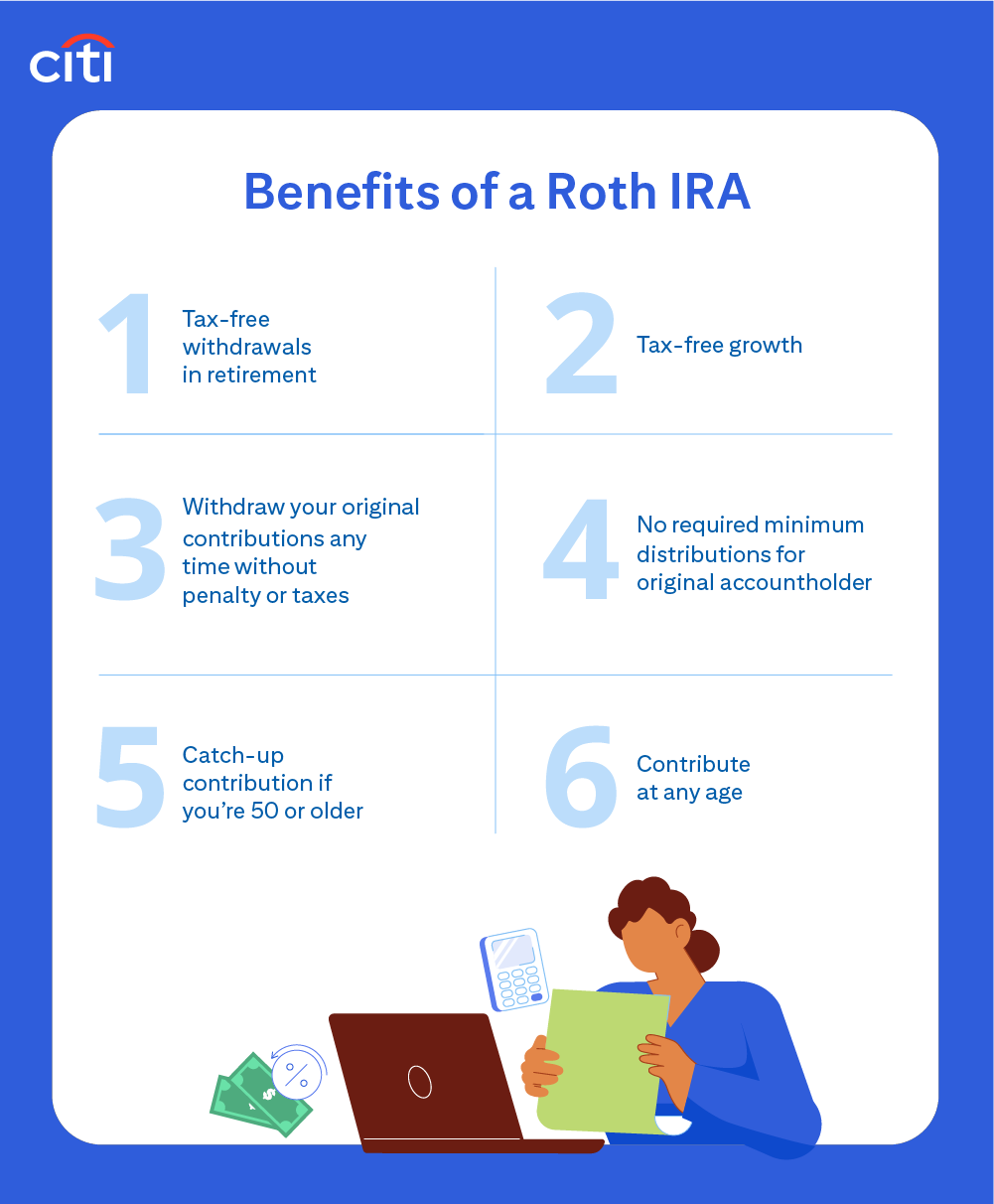

1. Growth and withdrawals are tax-free

With traditional IRAs, your contributions are tax-deductible, but your contributions to a Roth IRA are made with after-tax money.

Because your Roth IRA contributions are taxed, your withdrawals aren’t taxed if you meet certain requirements. You can make tax-free withdrawals after age 59 1/2 if your first contribution was at least 5 years ago, or if you otherwise meet the criteria for a qualified distribution.

2. Withdraw contributions penalty-free at any time

Roth IRAs have a required minimum age and time since your first contribution before you can withdraw your earnings without a tax penalty, but you can withdraw your contributions at any time without penalty. Your contributions include any initial deposits you’ve made, while your earnings include any interest or other growth.

3. No mandatory distributions apply to Roth IRAs

Required minimum distributions (RMDs) or mandatory withdrawals after a certain age do not apply to the original owners of Roth IRAs.

This is different from a traditional IRA, where distributions are required when you turn 73.

No RMDs mean that accountholders don’t have to withdraw money during market downturns and can let money grow for as long as they like.

4. No age limit for a Roth IRA

Roth IRAs don’t place age limits on contributions and distributions.

Your age does not prohibit you from contributing to a Roth IRA or Traditional IRA. This can allow you to catch up on retirement savings, particularly if you start saving later in life.